Emerging Markets in 2025: What consensus might have got wrong?

The alternative EM investment story for 2025

While we have often remarked that the asset class is the realm of optimists, the last decade has been challenging for Emerging Markets. A combination of US corporate exceptionalism, technological leadership, USD strength and a period of painful balance sheet repair in key markets has left it in the shadows. China’s re-adjustment and stumble into disinflation has transformed a central engine of global growth into an exporter of deflation. ROEs have suffered and MSCI Emerging Market’s returns have disappointed on account of its high index weightage.

However, the time to buy Emerging Markets is when the asset class is unloved and out of favour, when immediate catalysts are in play through pro-growth rate cuts, and when the corporate earnings story (USD denominated) begins to shine positively versus Developed Market peers. With US market outperformance against international equities reaching all time highs and with US equity risk premia touching all time lows, an asymmetric opportunity exists for the long-term, contrarian investor

2024 brought signs of structural improvement. Inflation - a longstanding Achilles’ heel for EM - has largely been tamed, creating room for pro-growth rate cuts. Moreover, EM’s return on equity (ROE) recovery and earnings per share (EPS) acceleration have outstripped those of Developed Markets for the first time in a decade. China, for so long afflicted by concerns about slipping into a deflationary spiral, began to make tentative signs that its pain threshold had been reached. There are clear signs that ‘credibly irresponsible’ fiscal support is being readied for the economy.

Still, significant questions remain. How will a potential Trump 2.0 presidency shape growth, inflation, trade, and geopolitics? Can China tackle its protracted battle with a high savings rate and thus excessive reliance on investment and exports. Are we likely to see credible intentions from policymakers to break free from the iron grip of overcapacity, excessive investment, and disinflation? And what degree of fiscal and monetary policy desynchronisation can markets expect between Developed and Emerging economies?

The bear case for EM in 2025 is well known: the US is expected to maintain tighter monetary policy, keeping the USD strong and financial conditions tight. This leaves EM with limited room for rate cuts despite improved balance sheets. Trade and tariff risks also loom large. However, these risks could be overstated, and we would point to four scenarios in which emerging markets can represent a compelling investment opportunity for this year and beyond

Trumps’s tariffs aren’t as bad as expected

The obituary of the EM asset class this year is framed around the prospect of aggressive tariffs disruptively introduced by Trump. However, the idea of 10-20% tariffs across the board and 60% on China isn’t necessarily certain. In fact, it may be unrealistic. First, ~50% of US imports consist of intermediate goods and draconian tariffs would be equivalent to taxing domestic manufacturers whilst penalising US exporters. Second, unrestricted tariffs will likely unleash an uncontrollable wave of retaliations by aggrieved parties (of which, there are many). Third, the underlying ambition of the incoming administrations seems to focus on ‘escalating to de-escalate’ – in essence, an aim to discuss threats, followed by negotiations, rather than imposing its will. We would view tariff threats more as a weapon to accelerate the unwinding of the ‘global economic reordering’ – essentially forcing other nations to lower savings (boost demand), flattening the competitive environment, raising US investment and productivity whilst reducing deficits. Perhaps average tariffs will double from 4% to 8% with further increments threatened. But this would be materially lower than the 20%+ rates deployed during the crisis of the 1930s. Emerging Markets assets will likely respond favourably to such an outcome

China’ self-help story gathers momentum

We have written extensively about the challenges China faces, and more importantly, our views on what can be done to reignite the investment story. China’s self-help story defines why it can be viewed as the contrarian bet for 2025. Whilst September 2024’s rally fizzled out following rounds of lukewarm policy updates, policymakers have revealed their pain threshold with a put now embedded in markets. Initiatives from other markets such as India, Japan and South Korea reinforce the importance of attracting a steady stream of domestic risk capital into their own markets. The wealth effect created by strong stock market performance is one of the mechanisms by which their uncomfortably high savings rate and low consumption intentions can be improved. We believe the key China related questions to consider in 2025 are:

- To what extent can the existing export led growth pivot to domestic consumption and still achieve the 5% GDP growth target?

- How persistent is deflation and how determined are policymakers to address the demand for money?

- How will authorities respond to a potential trade war?

The backdrop is supportive. Perhaps this year might see much awaited ‘credibly irresponsible’ fiscal support – particularly if US trade protectionism rears its head. Investor positioning is clean and the shift of capital sponsorship from DM to EM (particularly to China) will be material (some $45bn of inflows required to take global portfolios to market weight against benchmarks). Based on EPFR data, China allocations in mutual funds globally is at the 8th percentile, well down from the peak of 15% in 2020.9 Finally, corporate balance sheets are solid: with one of the highest cash to market cap ratios globally coupled with one of the lowest payout ratios.

Three investment themes stand out of us: 1) Companies to benefit from a domestic consumption revival; 2) Industrial policy support are well aligned with mid- cap sub-sector leaders and 3) Incumbents to benefit from industry consolidation and market repair (the China A-shares universe comprises of 5,300 companies with an $11 trillion market cap, compared to 5,800 companies in the US with a $49 trillion market cap.)

The global disinflation trend re-emerges and the USD weakens

We won’t profess to be experts in predicting the path of US inflation and where the implied Fed Fund Rate might settle. However, its impact on rates, USD and the outlook for EM is material. The volatility of moves has been suprising: 10Y bond yields have jumped to close to 5% whilst expectations of policy rates by Jan 2026 are now above 4%, implying one or two rate cuts over the next 12 months. Only four months ago, investors were expecting the Jan’26 Fed Fund rate to settle at 2.7% (and 10Y yields were 3.6%). This has been a remarkable, and painful, shift in expectations.

However, it is likely that the more structural drivers of disinflation will return – in particular, forces shaped by technological innovation, demographics, and debt levels. We see no reason for a sustainably higher r*(natural ratof interest). Indeed, more recent data points in Producer Price Index inflation has corroborated a renewal of this argument. As this gathers pace, the sensitivity on higher rates and a stronger USD will begin to dissipate. Again, this would represent a favourable outcome for the Emerging Markets asset class.

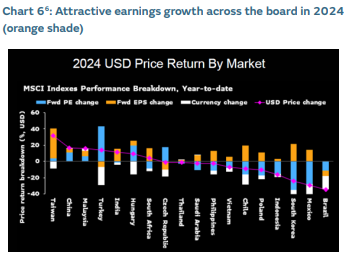

Pockets of Emerging Markets’ ROE revival story expand in size and durability

The corporate fundamentals story is perhaps the most important catalyst to re-rate Emerging Markets equities sustainably. Earnings projections for 2025-2027 highlight North Asia (with a focus on the semiconductor supply chain), South Africa and India as standout markets, whilst China remains most likely to see upside surprise (for reasons explained earlier). This now implies that Emerging Markets have seen earnings and ROE revisions that are outstripping developed markets for the first time in 13 years. The relative call between Emerging and Developed Markets now increases in importance. EM’s growing signs of improved corporate fundamentals strength is not fully discounted by markets.

As we look to 2025, history has a way of surprising us when consensus thinking becomes too entrenched. The four catalysts above provide a narrative on how 2025 could bring outcomes a little different than expected.

As always, the best opportunities often lie where few are looking.

This content should not be construed as advice for investment in any product or security mentioned. Examples of stocks are provided for general information only to demonstrate our investment philosophy. Observations and views of GIB AM may change at any time without notice. Information and opinions presented in this document have been obtained or derived from sources believed by GIB AM to be reliable, but GIB AM makes no representation of their accuracy or completeness. GIB AM accepts no liability for loss arising from the use of this presentation. Moreover, any investment or service to which this content may relate will not be made available by GIB to retail customers.